With the cost of living rising, it’s no surprise many people are noticing their insurance premiums creeping up too. We’ve had plenty of conversations with clients lately who are feeling that pressure.

If your premiums are starting to feel uncomfortable, it’s worth pausing before you cancel or strip everything back. Insurance is there to protect your family and your plans if something unexpected happens. The aim is to keep the right protection in place at a cost you can realistically maintain long-term.

This guide walks through practical ways to keep your premiums affordable, and when it helps to get advice before you make changes.

If you’re thinking about changing your cover, it’s a good idea to talk it through with an adviser first. A Lifestyle Solutions adviser can help you weigh up your options, understand the trade-offs, and make changes that fit your situation and budget.

Why insurance premiums rise over time

Premium increases usually come down to a few common factors. Many policies get more expensive as you get older. Inflation can also play a part – if your sum insured increases over time, your premiums often rise with it. And if you later change providers, any changes in your health or lifestyle can affect the terms you’re offered.

Your premium structure matters too. Stepped (age-rated) premiums typically start lower and increase each year as you age. Level premiums are usually higher at the start, but are designed to stay more stable over the longer term (unless you change your cover).

What can you do to reduce the cost of your cover?

Tip 1: Review your cover at least once a year

Insurance works best when it keeps pace with your life. What made sense a few years ago may not match your needs today. A simple annual review can help you spot cover you no longer need, features you’re paying for but don’t value, or areas where you may be over-insured.

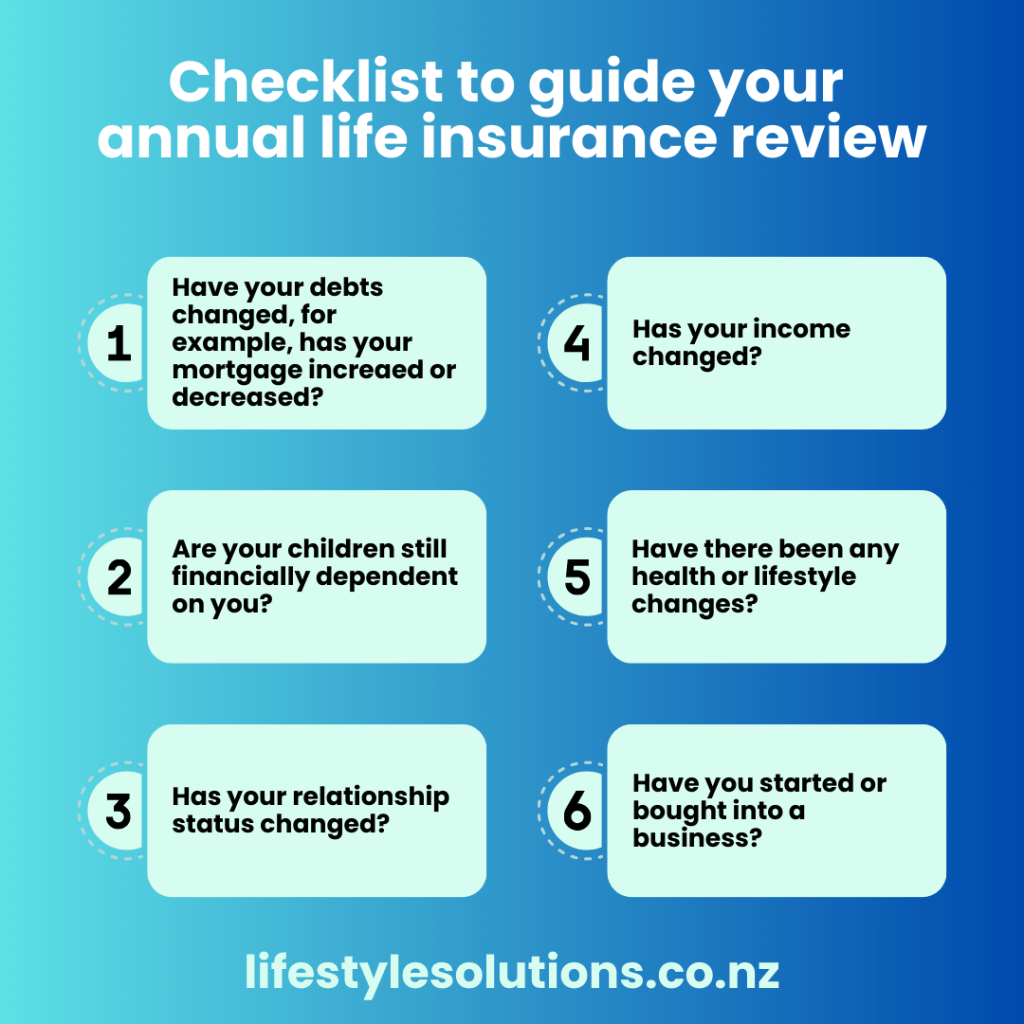

Here’s a quick checklist to guide your annual review:

- Have your debts changed (for example, has your mortgage increased or decreased)?

- Are your children still financially dependent on you?

- Has your relationship status changed?

- Has your income gone up or down?

- Has your savings or emergency fund grown?

- Have you started or bought into a business?

- Have there been any health or lifestyle changes?

- Which covers are ‘must-have’ for peace of mind, and which are ‘nice-to-have’?

Tip 2: Right size your cover

One of the biggest ways to reduce premiums is to adjust the sum insured so it matches your real goal. That doesn’t mean cutting corners, it means aiming for cover that makes life manageable, rather than trying to insure every possible dollar.

For example, imagine you have a four-bedroom home with a mortgage of $700,000. You might decide to reduce your life cover to $500,000. If one partner passed away, the surviving partner may not clear the mortgage completely, but the remaining balance could become manageable. And if downsizing is an option later, that could help close the gap. The key is that your plan still protects you from going backwards financially, while keeping premiums realistic.

Tip 3: Understand self-insurance (and use it strategically)

To ‘self-insure’ simply means you choose to cover some smaller risks yourself using savings or other buffers, and keep insurance for the big, life-changing risks.

Depending on your budget, self-insurance might look like:

- Using savings for smaller medical or dental costs

- Covering short-term income gaps with an emergency fund

- Choosing a higher excess on policies like car or home insurance

A helpful rule of thumb: avoid self-insuring anything that would seriously derail your finances – for example, long-term inability to work, a major illness without a safety net, or risks where others depend on your income.

Tip 4: Remove extra features you don’t need

Over time, it’s easy to accumulate add-ons and automatic increases that made sense at the time, but don’t add much value now. Review any optional extras and ask yourself: if this feature didn’t exist, would I pay extra to add it today?

- Optional riders or add-ons that increase cost without meaningfully improving your cover

- Automatic increases (for example, indexation) that no longer suit your budget

- Benefits you’re unlikely to claim on

Start with the essentials, then build extras back in only where they genuinely help

Tip 5: Adjust the settings that control cost

Different types of cover have different ‘levers’ that affect premium. A few common ones to consider are:

- Premium structure: check whether stepped or level premiums are the best fit for your budget and how long you expect to keep the cover.

- Waiting periods (for income protection): a longer waiting period can reduce cost, many people align this with how long their savings could support them.

- Benefit periods (for income protection): shorter benefit periods generally cost less, so it’s worth thinking about what you truly need to protect.

If you’re unsure which settings apply to your policy, this is where an adviser can be especially helpful, small tweaks can sometimes make a meaningful difference.

Tip 6: Compare providers carefully

Shopping around can help, but it’s important to compare like-for-like. Price is only one part of the story, policy wording, exclusions, limits and claim definitions matter too.

It can also help to remember that switching insurers may involve new underwriting, so any changes in health or lifestyle could affect what’s offered. A Lifestyle Solutions adviser can help you compare options properly and avoid unwanted surprises.

Tip 7: Lifestyle changes can lower premiums over time

Some lifestyle factors can influence premiums. If you smoke or vape, quitting can be one of the biggest steps you can take, it’s great for your health, and it may improve your insurance pricing over time. Managing underlying health conditions and keeping up with check-ups can help too.

Common mistakes to avoid when cutting premiums

- Making changes without advice – you may lose valuable benefits or end up under-insured

- Cancelling the most important cover first (instead of resizing it)

- Reducing cover without a plan to fill the gap, for example, savings or a downsizing plan

- Switching providers without understanding exclusions and definitions

- Letting policies lapse unintentionally

A simple action plan

If you’re not sure where to start, this quick step-by-step can help you narrow down what to review. You don’t need to do everything at once, even one small change can take the pressure off your budget.

1. List your covers and what you’re currently paying.

2. Rank each cover as ‘must-have’ or ‘nice-to-have’.

3. Pick one cost lever to test (for example: reduce the sum insured, remove add-ons, or adjust waiting/benefit periods where relevant).

4. Compare options, including what your current provider can offer versus alternatives.

5. Write down what you decided and set a reminder to review again next year.

Final Takeaway

Keeping premiums affordable comes down to being intentional. Review your cover regularly, right-size it to match what you actually need, self-insure smaller risks where it makes sense, remove extras that don’t add value, and compare providers carefully. The goal isn’t the cheapest premium – it’s cover you can keep in place, so you and your family are protected if something happens.

If you’d like a hand working through your options, a Lifestyle Solutions adviser can guide you through the best approach for your needs and help make sure any changes still leave you properly protected.

Ready to explore your options?

A quick conversation can bring real clarity. If you’re looking to review your life insurance cover, we’re here to help, professionally, transparently, and with a personal touch.

Disclaimer: The information contained in this blog is an overview and general information only. It may not be relevant to your individual circumstances. Before making any investment, insurance or financial planning decisions, based on information provided in this blog, please use your discretion and consult a professional adviser first. You can read our full disclosure statement here.

Frequently asked questions

How often should I review my life insurance?

At least once a year, and anytime something major changes (new mortgage, new baby, separation, income change). Regular reviews help keep cover aligned to your real needs and budget.

What does “self-insure” mean?

It means covering smaller costs yourself (usually with savings) while keeping insurance for the big, life-changing risks. It can be a smart way to lower premiums—when done carefully.

Is it risky to reduce my sum insured?

It can be if you cut too far. A safer approach is to reduce cover to a level that still keeps your household financially stable (for example, making the mortgage manageable rather than fully paid off).

Should I switch providers to get a cheaper premium?

Sometimes—but it’s important to compare like-for-like (definitions, exclusions, and benefits), not just price. Switching can also mean new underwriting, which may affect what you’re offered.

What’s the difference between stepped and level premiums?

Stepped premiums usually start lower and rise as you age. Level premiums typically cost more upfront but are designed to be more stable over the long term (though they can still change if you change your cover).

Can a Lifestyle Solutions adviser help me lower my premiums?

Yes, an adviser can help you weigh up options (like resizing cover or adjusting settings) and understand trade-offs, so you reduce costs without accidentally losing important protection.